Britain’s inflation rate fell in its last reading, but remains well above Bank of England targets. By the weird alchemy of economics, that all means that a property abroad suddenly cost more last week. Here’s why, and what could happen next.

Inflation in the past year or so has rocketed to levels not seen for 40 years. The good news is that more recent figures from the Office for National Statistics (ONS) show that inflation seems to have peaked and is slowly on the decline. This is much as the Bank of England (BoE) predicted. Moreover, they see it continuing to fall, dropping by more than half by the end of the year and even below the 2% target given to the central bank by the government.

As the Bank explained: “There are signs that inflation might now have turned a corner and begun to fall a little. We need to make sure it continues to fall and stay low. We expect inflation to begin to fall from the middle of this year and be around 4% by the end of the year. We expect it to continue falling towards our 2% target after that.”

Inflation measures

Every month, the Office for National Statistics (ONS) releases data on inflation, showing how much consumers are spending on goods and services in the UK.

There are a bewildering range of inflation records, but the two of most importance to the currency markets are:

- CPI inflation. The Consumer Price Index includes all the things that a household spends its money on, including food and energy prices, which are viewed as especially changeable.

- Core inflation. This excludes food and energy, and so offers a less volatile measure. Of course, all goods tend to be created using energy, and transported to shops using fuel, so they are still connected, but it still offers a better guide to underlying price trends.

The most recent UK data shows that the annual CPI rate fell to 10.1% in January, (below the levels that analysts had predicted, which was 10.3%). While this was its lowest levels in over six months, it is still well above the Bank of England’s target of 2%.

How inflation impacts the pound

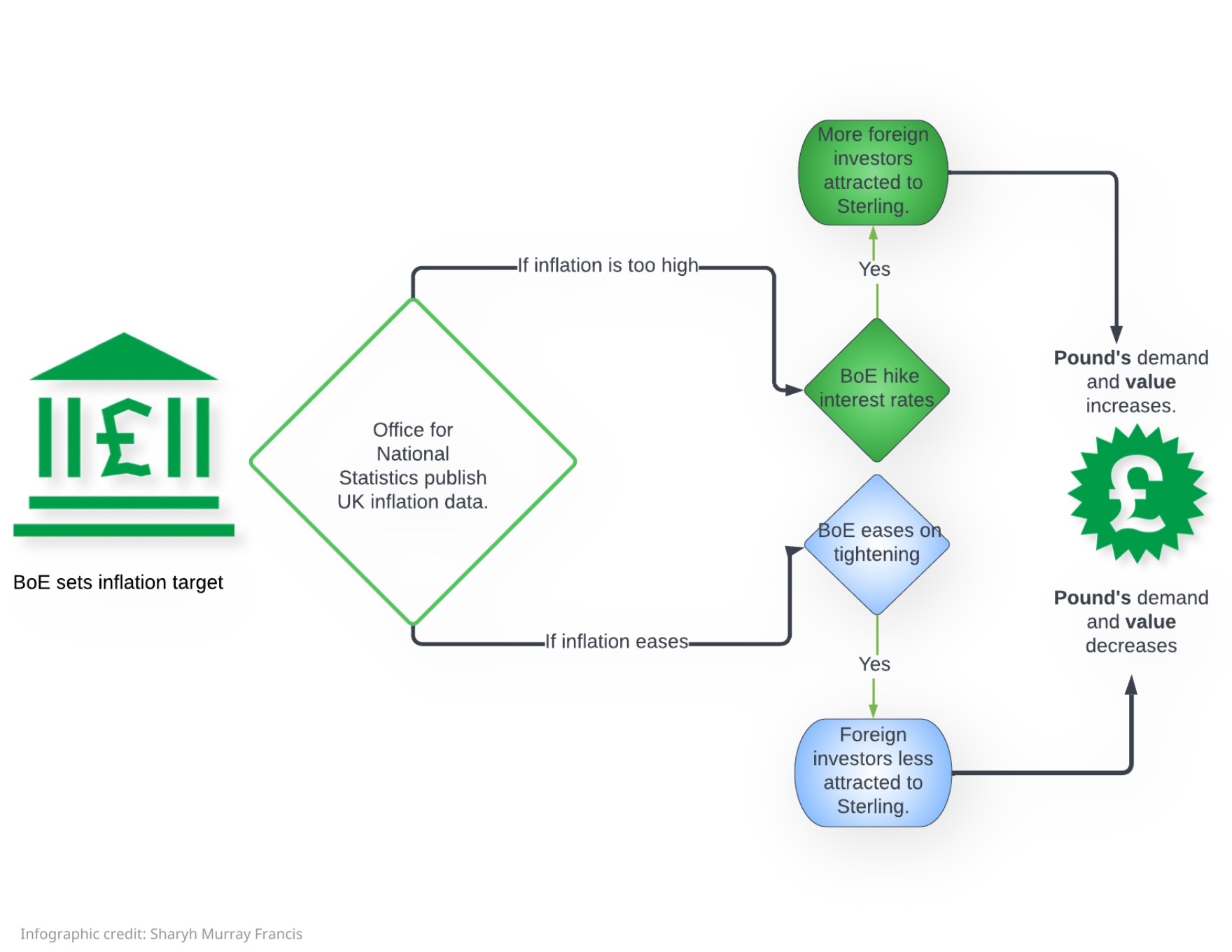

Inflation rates are among the biggest influences on exchange rates. That’s because the independent Bank of England is charged by the Chancellor of the Exchequer with keeping inflation to around 2%.

It does that by raising and lowering interest interest rates, which effectively puts in and takes out money from people and business’s pockets. If interest rates rise, people and businesses have less to spend, and so demand for goods and services falls and prices fall.

However, if interest rates rise, what happens to the money that businesses and people no longer have to spend? The organisations earning the extra interest are investors in UK assets, so when interest rates rise, more money pours into sterling and the strength of the pound rises.

Conversely, if inflation falls, the central bank can ease off on interest rates, or even lower them. Then, investors get a lower return from sterling and go and find another currency to invest in.

It is this interplay of investors vs interest rates, set by the central banks, influenced by inflation, that has a powerful effect on exchange rates.

The infographic below demonstrates how inflation data could impact the pound’s rates:

If inflation falls to 9.6% at the next announcement on 22nd March, (as markets are expecting) this would be the fourth consecutive decline and the BoE would find it difficult to make a case for continuing to raise (or “tighten”) interest rates. Where the Bank raises interest rates sharply to control inflation this is termed hawkish, and where it softens its stance and eases on rate rises it is dovish.

Can inflation impact my overseas transactions?

High inflation can impact a range of issues related to your overseas purchase and lifestyle. For one, high inflation devalues your savings. More immediate will be the effect on your exchange rate. There are two sides to an exchange rate and it has been the more hawkish stance in recent weeks from Europe and America’s central banks, the European Central Bank (ECB) and the Federal Reserve, that has damaged GBP/EUR and GBP/USD.

The Bank of England’s counterparts in the ECB have the additional challenge of balancing dozens of countries’ inflation rates. In recent months these have ranged from as much as 21% in some Baltic states to around 6% in Spain and France.

So should it risk damaging the larger economies by hiking interest rates? Its strategy of slow but steady interest rate rises may be keeping the economy growing marginally faster than the UK’s, but it may not be enough to fight inflation. Spain’s rate climbed slightly to 6.1% in February, Germany’s to 8.7%, while Italy’s fell to 9.2%. In France the rate edged higher to 6.2% in February. Food, services and manufactured products prices rose the most.

Where will the ECB go next, and what will happen to inflation rates? The fact is that no-one knows and no-one can predict exchange rates either. That is why we advocate a safety-first approach. Please get in touch with one of our team on 020 7898 0541 to discuss your options. We’d be delighted to help.