What do you need to know when making a large GBP to EUR transaction? When buying property in the eurozone, most buyers choose to protect their future from currency risk, with a forward contract.

While buying a property overseas can be exciting, the fulfilment of a long-cherished dream, there are several stages in the process and few of them are entirely stress-free. After all, you are sending a very large amount of money, saved over many years, into another country, currency and legal system.

The good news is that the legal process – and the protections offered by the legal systems within our favourite buying destinations – tend now to be clear, honest and simple to navigate (using a good lawyer, of course).

Download your free guide, the Property Buyers Guide to Currency.

But the currency transaction still poses risks. Why is that? In two words: currency risk.

What is currency risk?

Currency risk arises from currency volatility.

Currency = [noun] a system of money in general use in a particular country.

Volatility = [noun] liability to change rapidly and unpredictably, especially for the worse.

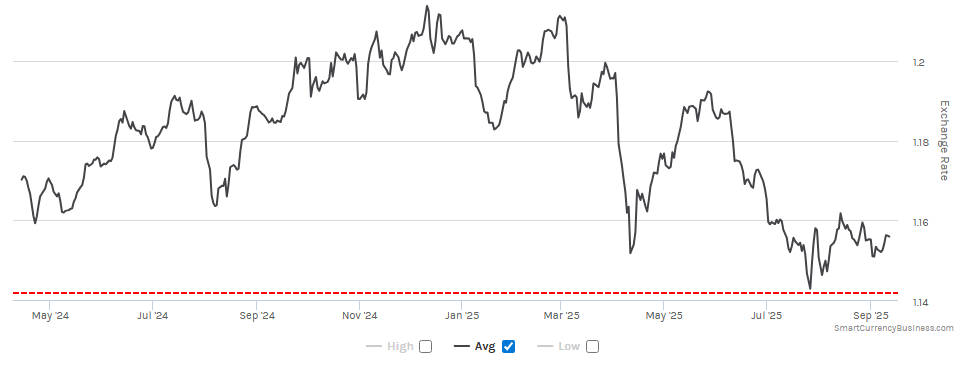

In practical terms currency volatility means the tendence of an exchange rate to weaken or strengthen, either over time or sharply. This is a typical exchange rate, the pound to euro rate over a year.

GBP/EUR over one year

If GBPEUR moves during your property buying process, when you have committed to a purchase in Spain, France, Portugal, Italy, Ireland or elsewhere and even paid a deposit, you will not know what you will have to pay in pounds.

What causes currency volatility?

Most exchange rate movements, certainly between the pound and euro, are driven by supply and demand. Investors buy and sell vast quantities if currency every day. About $10 trillion of currency is traded globally every day, which is roughly equivalent to the entire value of every home in the UK.

Those flows are investors looking for a better return on their capital, so they are looking for the best interest rate, the fastest growing economy, the most politically stable country. In practice, for GBPEUR that means that exchange rate will be influenced by:

- European Central Bank (ECB) interest rate decisions

- Bank of England (BoE) interest rate decisions

- Inflation and unemployment announcements

- Economic growth data

- Political developments, such as elections

- Financial sentiment, such as business confidence surveys

Then there are those events we tend to nickname ‘black swans’ – unexpected and unpredicted, such as the pandemic, the wars in Ukraine and Iran, or Brexit.

The key takeaway is that all of these factors are outside your control.

You may notice that GBP/EUR tends to rise slowly and fall rapidly. That’s to do with what underlies the strength of a currency. GBP is viewed as more volatile than EUR and is an additional risk for UK buyers in the eurozone.

Why GBP to EUR volatility matters for property buyers

If you are buying euros for an overseas property purchase, your exposure to currency volatility begins the moment your offer is accepted.

- A 1% movement on €300,000 can materially change your sterling requirement

- A 3% shift can equal several thousand pounds

- A 10% shift on an averagely priced property (€300,000) will change the price you pay, up or down, by around £30,000.

The issue for property buyers is the length of time that an overseas purchase can take. A two-to-three -month purchase timeline is perfectly normal.

You will normally be committed to paying a price in euros from the moment your offer is accepted, or at least from when you sign a preliminary contract and pay a 10% deposit. But you will not pay the rest of the money (~90%) until the lawyers have finished their work, usually at least two months later.

A lot can happen in that time. If you look at the graph above, you can see sharp falls. In the six weeks between early March and mid-April GBP/EUR weakens from 1.21 to 1.15. So if you had committed to a payment of €300,000 in March and had to pay in April you might have needed to find another £13,000.

Of course, the currency could go the other way and you find on completion day that you have an extra £13,000. However, that is a risk that few buyers wish to make.

What is the solution to currency risk?

The solution is to “hedge” your exposure. Hedging is, quite literally, putting a barrier around your potential losses. In financial terms it means locking in a return or a deal in advance, rather than leaving it up to the market.

With euros for a European property purchase, the most common hedge is a forward contract.

The definition of a forward contract is a legally binding agreement that fixes your exchange rate today for a transfer that will occur in the future.

For euro property purchases, this means:

- You lock in your gbp to eur rate

- You remove uncertainty before completion

- Your sterling budget becomes fixed

This is not speculation; it is structured way of removing (mitigating) your risk.

So if you were making a firm offer on that €300,000 house, you would speak to Smart Currency and agree a rate, based on that day’s rate – for example, you lock in that amount at €1.15 meaning . Then when you complete maybe three months later, you know you will pay £261,000.

If when you complete on the purchase the interbank rate has dropped to €1.10 you would have had to pay an extra £11,000 without the forward contract.

Why many buyers choose certainty

Property buyers, especially those in mid to later life often prioritise clarity over their budget. It protects their capital and reduces stress. Rather than monitoring the exchange rate each day, they can relax and look forward to owning their new property in Europe.

Comparing ways to buy euros

| Option | Forward Contracts | Personal Support | Suitable for Large Property Transfers |

| High street bank | Often limited | Call centre | Possible but limited structured planning |

| Digital provider | Rarely available | App based | Designed for transactional transfers |

| Smart Currency Exchange | Available for retail buyers | Dedicated named account manager | Specialist in overseas property |

The key difference is not simply the quoted rate. It is access to structure, support and certainty.

Important clarification

Smart Currency Exchange does not provide travel cash or holiday money. We specialise exclusively in secure international bank transfers for larger transactions. If you are ordering €500 for a weekend break, this is not our service. If you are transferring €300,000 for a property purchase, this is precisely our focus.

Regulatory and trust framework

For many buyers, reassurance is critical. Smart Currency Exchange offers:

- FCA authorisation

- 2000+ excellent Trustpilot reviews

- Official partnership with Zoopla, Your Overseas Home and other property professionals

- Segregated client accounts

- No transfer fees for transfers over £3,000.

For clients transferring substantial sums, these factors matter.

When should you fix your euro rate?

Forward contracts are typically appropriate when:

- You have a fixed completion date

- You are transferring a large sum in the future

- You cannot afford adverse movements

- Your budget is tightly structured

- You prioritise certainty over speculation

They may not suit every scenario. But for property purchases, they are frequently central to risk management.

Frequently Asked Questions on GBP to EUR transactions

Because exchange rate changes are unpredictable, waiting is no guarantee of a better exchange rate. Waiting simply exposes you to further market movement, whether favourable or unfavourable. If you have a fixed completion date, securing certainty may be more important to you than attempting to time markets. However, this is a personal choice and at Smart Currency we do not offer financial advice.Is it better to wait for a better exchange rate?

Some banks may offer limited access. Availability and flexibility can vary. Structured specialists typically provide more tailored support.Do banks offer forward contracts to retail clients?

No. Smart Currency Exchange does not charge transfer fees on transactions over £3,000. Smart Currency takes its customer care duties extremely seriously. You can see how it fulfils these <a href=”https://www.smartcurrencyexchange.com/legal/consumer-duty/”>customer care responsibilities here</a>.Does Smart Currency charge transfer fees?

Yes. Smart Currency Exchange is authorised by the Financial Conduct Authority (FCA) under the Payment Services Regulations 2017 for the provision of payment services. If you’d like to confirm our FCA authorisation, please visit our listing on the <a href=”https://www.fca.org.uk/consumers/fca-firm-checker/firm-10531-504509″>FCA’s Financial Services Register</a>. Our reference number is: 504509. We are also members of two industry trade associations: the UK Money Transmitters Association (UKMTA) and the Association of Foreign Exchange and Payment Companies (AFEP). These were established to ensure shared high standards across the money transfer industry.Is Smart Currency officially authorised?